Prediction: Foundation Model Leaders Shift Focus to AI Applications

In 2025, the generative AI ecosystem is entering a transformative phase, with leading frontier labs like OpenAI, Anthropic, Cohere, and xAI poised to redefine their priorities. Traditionally focused on building and refining cutting-edge foundational models, these organizations are now shifting their attention “up the stack” to concentrate on AI-driven applications. This strategic pivot reflects their need to capture new revenue streams, differentiate their offerings, and maintain competitive advantages in an increasingly crowded and commoditized market.

This evolution comes at a time of intense competition. Alongside frontier labs, major tech giants like Google, Microsoft, and Meta are investing heavily in AI applications, leveraging their expansive ecosystems to deliver integrated solutions. Meanwhile, specialized startups such as Perplexity, Harvey, and Sierra are rapidly gaining ground by offering niche, application-specific tools that challenge the dominance of larger players. Some organizations have already begun to explore this space, with examples like OpenAI’s phone services, its integration with Microsoft’s Azure OpenAI Service, and Anthropic’s enterprise-focused chatbot tools leading the charge.

As the battle for the application layer intensifies, success will hinge on the ability to create impactful, real-world solutions that address both enterprise and consumer needs. This new era of generative AI will be defined by innovation, differentiation, and the strategic navigation of a fiercely competitive landscape.

This article is part of a larger series titled “AI and Language Processing Predictions for 2025.”

Each prediction topic in the series is accompanied by a detailed article that explains the prediction, along with the necessary background information to provide context and depth.

Challenges in Foundation Model Development

Building and scaling foundation AI models remains one of the most resource-intensive endeavors in the technology landscape. Organizations like OpenAI, Anthropic, xAI, and Meta have poured billions into creating state-of-the-art generative AI systems, with costs escalating dramatically as the demand for more powerful and sophisticated models grows.

For example, OpenAI’s record-breaking $6.5 billion in funding highlights the sheer financial resources required to sustain such efforts. Meta’s $40 billion AI investment further underscores the scale of capital needed to develop and deploy cutting-edge models like Llama 3 and 4. Similarly, Anthropic and xAI face steep financial commitments, as evidenced by the delayed rollout of flagship models such as xAI’s Grok 3 and Anthropic’s Claude 3.5 Opus.

The case of Grok 3, xAI’s ambitious next-generation model, exemplifies the challenges foundation model pioneers face. Initially promised by Elon Musk to launch by the end of 2024, Grok 3 remains missing as of January 2025, with signs suggesting an intermediate model, Grok 2.5, may arrive first. Musk himself acknowledged the difficulty of achieving such goals, pointing to scaling limitations and the immense complexity of training state-of-the-art models. Similarly, Anthropic scrapped plans to release its Claude 3.5 Opus model in 2024, reportedly due to economic impracticality, despite completing the training process.

These delays reflect a growing trend of unmet deadlines and scaling challenges, underscoring the limitations of current AI training methodologies. In the past, significant performance improvements could be achieved by training on massive datasets with increasing computational power. However, the gains with each new generation of models are shrinking, making it harder to justify the soaring costs of development.

Challenges include:

- Diminishing Returns on Data: As high-quality datasets become scarcer, achieving meaningful improvements in model performance becomes increasingly difficult and expensive. Models now require exponentially larger datasets and advanced preprocessing techniques to deliver incremental gains, driving up both time and resource costs.

- Escalating Capital Costs: Foundation model development is critically dependent on expensive hardware, particularly semiconductors. Nvidia GPUs dominate the generative AI revenue stack, capturing 83% of the total value with gross profits exceeding 88%. This reliance on high-cost hardware creates significant barriers to entry and limits scalability, especially for smaller players. For example, xAI’s Grok 3 required training on a cluster of 100,000 H100 GPUs, each costing $30,000, or $3 billion just for hardware alone—a staggering investment for any organization.

- Low Customer Loyalty: Many AI applications are model-agnostic, meaning customers can easily switch providers based on price, performance, or feature set. This low customer stickiness undermines long-term revenue stability for foundation model pioneers, especially as competition intensifies.

- Emerging Competition from Open Models: Open-source alternatives like Meta’s Llama 3 and 4 and Alibaba’s Qwen are gaining traction. These models offer high performance at a fraction of the cost, posing a direct threat to foundation model pioneers’ premium offerings. The increasing adoption of open models has also driven commoditization, further eroding profit margins for proprietary models.

- Operational Complexity and Delays: The development of foundation models involves immense technical and logistical complexity. Delayed launches, such as those of Grok 3 and Claude 3.5 Opus, highlight the growing bottlenecks in training, fine-tuning, and deployment.

The Sustainability Problem

These challenges highlight a growing issue: foundation model development as a standalone business is becoming increasingly unsustainable. The combination of skyrocketing costs, diminishing performance returns, low customer loyalty, and stiff competition is forcing labs to reevaluate their strategies. Many are now shifting “up the stack” to focus on AI applications as a way to capture higher margins, differentiate their offerings, and ensure long-term viability.

The Three Phases of Value Migration in Generative AI

Phase 1: Hardware Dominance (Today)

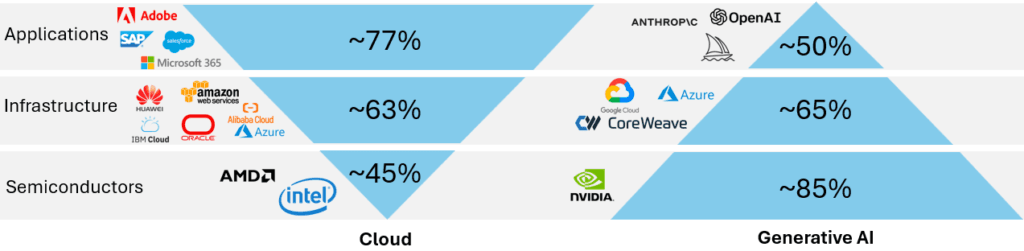

- Semiconductors as the Core Driver: Nvidia GPUs dominate, capturing 83% of Gen AI revenue and 88% of gross profits.

- Capital-Intensive Model Development: Billions of dollars are required for hardware and computational resources to train models like OpenAI’s GPT-4 or xAI’s Grok 3.

- Challenges in Foundation Model Development:

- Escalating costs for training and hardware.

- Diminishing returns on data improvements.

- Operational complexities and delayed rollouts (e.g., Grok 3 and Claude 3.5 Opus).

- Market Characteristics: High competition between proprietary models and emerging open models like Meta’s Llama.

Phase 2: Infrastructure and Ecosystem Integration (Short-Term Transition)

- Shift “Up the Stack”: Foundation model pioneers (e.g., OpenAI, Anthropic, xAI) begin integrating foundational models into enterprise ecosystems to capture new revenue streams.

- Cloud Convergence: Cloud providers like AWS, Azure, and Google Cloud incorporate AI capabilities into their infrastructure, blurring boundaries between AI and cloud ecosystems.

- Emerging Enterprise Solutions:

- AI-driven customer service platforms.

- Industry-specific tools in healthcare, legal, and finance.

- Integration of AI models into broader workflows.

- Risks: Increased competition from hyperscalers, application developers, and open-source models, as well as potential conflicts with existing customers.

Phase 3: Application Layer Dominance (Next 10 Years)

- Applications as the Largest Growth Driver:

- Applications, currently only 6% of Gen AI revenue and 3% of profits, are projected to dominate value creation and gross profits, following patterns seen in mobile and cloud ecosystems.

- Custom AI applications will offer higher margins, deeper customer engagement, and tailored industry solutions.

- Historical Parallels:

- Mobile ecosystem: Value shifted from hardware (e.g., Qualcomm) to applications (e.g., iOS/Android).

- Cloud ecosystem: Applications now account for 67% of profits compared to semiconductors’ 5%.

- Key Benefits of Applications:

- Higher gross margins.

- Stronger differentiation through vertical-specific solutions.

- Stickier revenue streams via direct user engagement.

- Business Imperative: Companies that invest in building AI applications today will capture future growth as Gen AI applications become a cornerstone of competitive advantage.

A Deep Dive Into The Application Layer: A New Frontier

As the generative AI ecosystem matures, leading foundation model pioneers like OpenAI, Anthropic, and xAI are making a strategic shift toward the application layer, marking a significant evolution in their business models. This move mirrors patterns observed in other industries, such as the semiconductor and cloud ecosystems, where value transitioned from foundational layers—hardware and infrastructure—to the application layer as markets mature. By focusing on applications, these labs aim to capture higher margins, create differentiated offerings, and establish more enduring customer relationships.

Why the Application Layer?

The pivot to applications addresses several key challenges faced by foundation model pioneers in foundational model development:

- Economic Sustainability: Foundational model development is resource-intensive and increasingly unsustainable as standalone businesses. Training large-scale models like OpenAI’s GPT-4 or Anthropic’s Claude requires billions in funding, massive computational resources, and high-quality datasets that are becoming scarcer.

- Market Differentiation: Applications provide a means to stand out in a crowded and commoditized market. With open models like Meta’s Llama and Alibaba’s Qwen gaining traction, proprietary foundation models face growing competition. The application layer allows labs to offer unique, tailored solutions that leverage their models’ capabilities in ways competitors cannot easily replicate.

- Stickier Revenue Streams: Unlike foundational models, which often serve as interchangeable components in broader AI solutions, applications create direct relationships with users. First-party applications such as OpenAI’s ChatGPT demonstrate how labs can build customer loyalty by offering end-to-end solutions.

- Lessons from Other Industries: In both the semiconductor and cloud ecosystems, initial value accrued in hardware and infrastructure. However, over time, software and applications became the primary drivers of revenue and profit. For instance, Nvidia, a leader in semiconductors, has expanded into AI frameworks like CUDA and cloud-based tools to diversify its revenue. Similarly, cloud providers like AWS, which began with infrastructure, now derive significant revenue from SaaS applications and integrations.

- AI as a Competitive Advantage: Generative AI is rapidly becoming a cornerstone for businesses aiming to stay competitive. By integrating AI into enterprise software, organizations can transform content creation, customer engagement, and workflow optimization. These advancements not only enhance operational efficiency but also enable businesses to achieve significant cost savings and scale rapidly with minimal resources. Companies that strategically adopt AI-driven processes will find themselves at the forefront of their industries, while those that neglect it risk falling behind in an increasingly AI-powered marketplace.

The Generative AI Stack: How Value Migrates to Applications

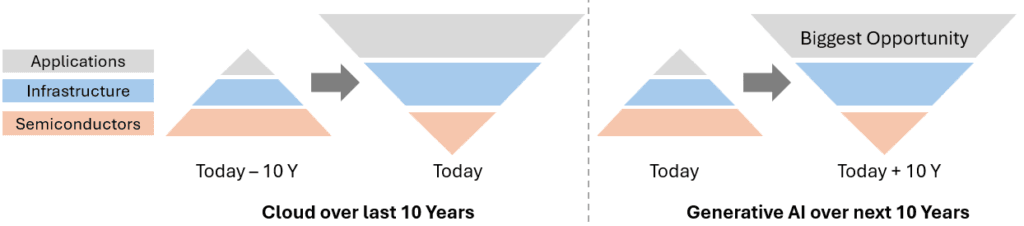

Over the past two years, the Generative AI (Gen AI) market has experienced an “iPhone moment”—a period of rapid adoption and transformative recognition. As the market matures, the value captured by the Gen AI stack is segmented into three primary layers: semiconductors, infrastructure, and applications. Currently, semiconductors dominate both revenue and profit, but historical patterns in technology ecosystems suggest this will not last.

Case Study: Mobile and Cloud Value Shifts

Historical technological shifts provide a clear precedent for value migration within maturing ecosystems.

- Mobile Wave: Initially, value in the mobile ecosystem accrued in semiconductors, driven by chipmakers like Qualcomm. As the market matured, infrastructure such as mobile networks gained prominence, eventually giving way to applications like iOS and Android, which now dominate value creation.

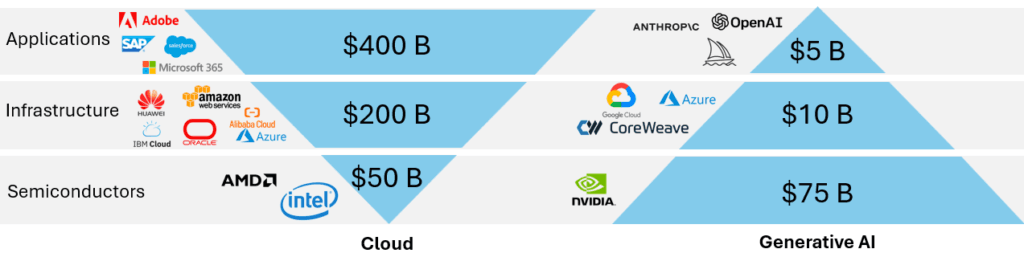

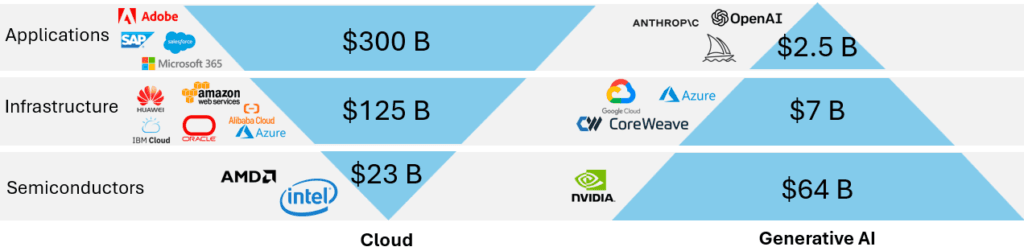

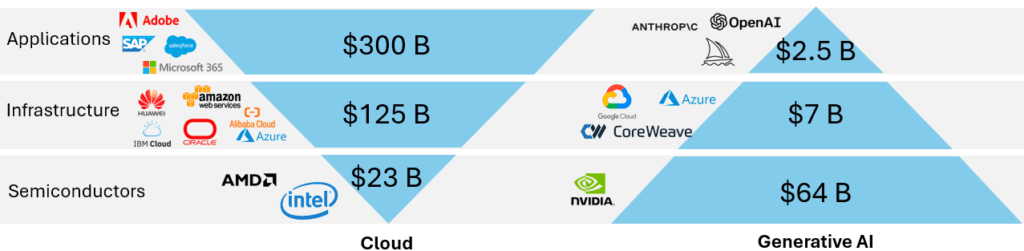

- Cloud Ecosystem: In the early 2000s, the cloud ecosystem focused heavily on data center hardware and cloud infrastructure. By 2010, companies like AWS led the shift toward scalable cloud services. Applications like Salesforce and Adobe eventually emerged as the dominant profit centers, accounting for 67% of gross profits, or approximately $300 billion annually.

Generative AI is expected to follow a similar trajectory, with a current focus on hardware (Phase 1). Over the next decade, applications (Phase 3) are anticipated to drive the majority of value as AI adoption scales and matures.

Hardware Dominance Today

Semiconductors currently dominate the Generative AI stack:

- Revenue Capture: Semiconductors, primarily Nvidia GPUs, account for 83% of Gen AI revenue.

- Profit Accrual: Semiconductors capture 88% of gross profits, mirroring the early days of the semiconductor industry with companies like Intel and AMD.

Gen AI Revenue Distribution

In comparison, Gen AI applications—like ChatGPT and MidJourney—account for just 6% of revenue and 3% of profits. This disparity echoes the early days of the PC ecosystem, where foundational hardware overshadowed software.

Applications: The Next Frontier

As with mobile and cloud ecosystems, the application layer represents the largest untapped opportunity in Generative AI. Applications are expected to transition from early-stage growth to become the dominant driver of both revenue and profits.

Key Benefits of Applications

- Higher Margins: Applications inherently have higher gross margins than foundational models or hardware.

- Greater Differentiation: Tailored solutions for healthcare, legal, and customer service can establish competitive advantages.

- Stronger Customer Relationships: Direct engagement with end-users fosters loyalty and creates recurring revenue streams.

Projected Growth of Applications in Gen AI

Comparison with Cloud Ecosystem

- In cloud computing, semiconductors contribute only 5% of gross profits, while applications drive 67%, or $300 billion annually.

- Gen AI, by contrast, is at an early stage where semiconductors capture the overwhelming majority of profits.

Comparison of Profit Accrual in Cloud vs. Gen AI

The Biggest Opportunity: The Application Layer

The application layer represents the greatest untapped potential in Generative AI. As businesses increasingly adopt and scale Generative AI technologies, applications are poised to become the primary drivers of value creation, positioning themselves as the key growth area in the years ahead. This shift mirrors earlier technological waves, such as the mobile and cloud revolutions, where applications ultimately emerged as the largest contributors to value creation.

Currently, applications account for just 6% of revenue and 3% of profits in the Generative AI market. This dynamic is reminiscent of the early PC era, where hardware initially dominated while software’s potential was underappreciated. Over time, however, software evolved into the primary value driver—a trajectory that Generative AI applications are expected to replicate.

Evolution of GenAI Stack Over Next 10 Years

As the market matures, value is expected to shift “up the stack” from semiconductors and foundational models to applications. Historically, we’ve seen similar patterns: in the semiconductor industry, value migrated from hardware to software products like Windows and Photoshop. Likewise, in Generative AI, applications such as ChatGPT and enterprise solutions are anticipated to dominate both revenue and profit in the coming decade.

Evolution of Value Accrual in Semiconductors and AI

This trajectory underscores how Generative AI is likely to follow the same path, with applications emerging as the primary growth and profit driver.

For businesses, this transition from hardware-centric to application-centric value in Generative AI presents a pivotal opportunity. Companies that strategically invest in AI-driven software and applications today will be well-positioned to capture exponential growth as the market evolves.

As cloud and AI technologies continue to converge, the boundaries between cloud infrastructure and AI applications will blur, further accelerating this transformation. To stay competitive, businesses must prioritize developing and integrating AI-powered applications that fully leverage the potential of this evolving ecosystem.

Comparison with the Cloud Ecosystem

The revenue distribution in the Generative AI stack differs significantly from the traditional cloud ecosystem, highlighting the early dominance of hardware in Gen AI compared to the mature application-driven cloud market.

- Semiconductors in Cloud: In the traditional cloud market, semiconductors contribute only 5% of gross profits. This contrasts sharply with Gen AI, where semiconductors capture a dominant 88% of gross profits.

- Applications in Cloud: Applications drive 67% of gross profits in the cloud ecosystem, generating approximately $300 billion annually from leaders like Salesforce and Adobe. In Gen AI, applications are in their infancy, contributing just 3% of gross profits, or $2.5 billion.

This disparity underscores the nascent stage of Gen AI applications, which are expected to grow substantially as the ecosystem matures, mirroring the cloud market’s evolution toward application-driven value.

The profitability distribution within the Gen AI ecosystem highlights a heavy reliance on hardware as the core enabler of AI advancements, compared to the cloud ecosystem, where applications dominate with 67% of total gross profits. As the Gen AI market matures, the distribution of profits is expected to shift, with infrastructure and applications capturing a larger share as AI adoption scales across industries.

However, for the time being, semiconductors remain the primary driver of profitability in the Gen AI stack, capturing the overwhelming majority of gross profits. This heavy reliance on hardware is expected to persist until AI applications increase their monetization strategies and broaden their contribution to the value chain.

Additionally, as cloud and Gen AI continue to evolve, crossovers between the two ecosystems are expected. Cloud providers such as AWS, Azure, and Google Cloud are already integrating AI capabilities into their infrastructures, offering AI services as part of their broader cloud offerings. This convergence will blur the lines between the two ecosystems, creating new opportunities as AI becomes embedded into cloud infrastructures and applications.

The Benefits of the Pivot

By focusing on applications, foundation model pioneers can unlock several strategic advantages:

- Higher Margins: Applications typically command higher gross margins than foundational models, which are costly to develop and maintain. By moving “up the stack,” labs can transition from low-margin infrastructure dependencies to high-margin software solutions.

- Greater Differentiation: Applications allow labs to create tailored offerings, addressing specific needs in industries such as healthcare, legal, and customer service. This differentiation can establish competitive advantages that are difficult to replicate.

- Stronger Customer Relationships: Direct engagement with end-users through applications fosters loyalty and creates opportunities for ongoing revenue through subscriptions, premium features, and integrations.

Potential First-Party Applications

foundation model pioneers are well-positioned to expand their application offerings across both enterprise and consumer markets. There are already many examples of this happening with third-parites and the many foundation model pioneers will enter the market with both new offerings and competition

Enterprise Solutions

- Search Applications: Advanced search tools tailored to specific industries or workflows.

Example: OpenAI’s SearchGPT, integrated with Microsoft Azure OpenAI Service, supports enterprise search in legal and healthcare sectors. - Customer Service Platforms: AI-driven chatbots and virtual agents for resolving customer queries.

Example: Anthropic’s Claude AI integrates into customer support systems to deliver personalized, empathetic responses. - Legal and Sales AI: Tools for drafting contracts and automating sales pipelines.

Example: Harvey, built using OpenAI models, provides legal professionals with contract drafting and review assistance. - Healthcare Assistants: AI tools for diagnostics, treatment recommendations, and patient management.

Example: xAI’s Grok AI is designed to integrate with healthcare systems for advanced data analysis and diagnostics. - Finance and Accounting Tools: Automated solutions for financial reviews and compliance monitoring.

Example: OpenAI models are embedded in financial analysis tools like Klarity AI to streamline document reviews.

Consumer Products

- Personal Assistant Agents: Multifunctional assistants for task and schedule management.

Example: OpenAI’s ChatGPT Plus acts as a personal productivity assistant, integrated into various apps like Notion. - Generative Music and Art: Creative tools for personalized content generation.

Example: OpenAI’s DALL-E and Jukebox enable users to generate custom visuals and music. - Education and Training Tools: Adaptive learning systems for tailored education.

Example: Anthropic’s Claude is utilized in educational platforms to deliver personalized tutoring experiences. - Gaming AI: Adaptive AI for storytelling and NPC behavior in games.

Example: OpenAI’s ChatGPT API powers dynamic characters and storylines in games like AI Dungeon. - Health and Wellness Apps: Mental health and fitness tools.

Example: Wysa, a mental health app, incorporates OpenAI’s models to provide supportive and empathetic conversations. - Home Automation and IoT Integration: Smart systems for home management.

Example: OpenAI’s integrations with voice assistants like Alexa enhance home automation experiences. - Generative Content for Social Media: Tools for creating engaging visuals and captions.

Example: OpenAI’s DALL-E generates unique visuals for content creators.

Emerging and Niche Use Cases

- Environmental and Sustainability Tools: AI-powered platforms for sustainability efforts.

Example: foundation model pioneers like OpenAI are enabling startups to build sustainability tools leveraging their APIs. - Event Planning and Management: AI tools for event organization and logistics.

Example: OpenAI’s models are used in custom event planning applications for creating themes and managing workflows.

Challenges in the Pivot

While the pivot to the application layer presents significant opportunities, it is not without challenges:

- Direct Competition: foundation model pioneers now face competition not only from other labs but also from established application developers like Perplexity (search), Harvey (legal AI), and Sierra (customer service). These companies have already built strong customer bases and specialized tools that may compete directly with new first-party offerings.

- Managing Customer Relationships: Many existing application developers rely on foundational models from foundation model pioneers. By entering the application space, labs risk alienating these customers, potentially losing them to rival model providers.

- Integration Complexities: Developing and deploying applications often require integration with broader ecosystems, such as enterprise software or cloud infrastructures. This adds layers of complexity to the application development process.

Challenges in the Pivot to the Application Layer

The transition to the application layer opens up vast growth opportunities for foundation model pioneers but introduces a distinct set of challenges that require careful navigation. Increased competition from established players and specialized startups, shifting customer dynamics, and the technical intricacies of application integration pose significant hurdles. Success in this pivot will hinge on three critical factors: strategic differentiation, maintaining strong customer relationships, and achieving operational excellence. By addressing these challenges head-on, foundation model pioneers can secure their position as leaders in the rapidly evolving generative AI ecosystem.

1. Direct Competition in the Application Space

Foundation model pioneers now find themselves in a crowded application market, facing competition from multiple fronts:

- Specialized Startups: Companies like Perplexity (search), Harvey (legal AI), and Sierra (customer service) have established strong footholds in niche verticals. Their domain expertise and targeted solutions give them a competitive advantage over generalized applications from foundation model pioneers.

- Established Tech Giants: Companies like Google, Microsoft, and Amazon are leveraging their expansive ecosystems to integrate generative AI applications into their existing platforms, offering end-to-end solutions that are hard to rival.

- Open-Source Ecosystems: Open-source models, such as Meta’s Llama, enable smaller developers to build competitive applications without relying on proprietary foundation models. This broadens the competitive landscape and intensifies pressure on proprietary labs to justify their premium offerings.

Impact: Foundation model pioneers must differentiate their applications by offering unique features or seamless integrations that competitors cannot easily replicate. Failure to do so could lead to market share erosion.

2. Managing Customer Relationships

The pivot to applications introduces the risk of alienating existing customers who rely on foundational models to power their own offerings:

- Conflict of Interest: By developing first-party applications, foundation model pioneers may compete directly with the very developers who have built businesses around their models. For example, if OpenAI launches an AI-driven legal assistant, it could undercut startups like Harvey, which depend on OpenAI’s API for their services.

- Switching Providers: Alienated customers might migrate to alternative foundational model providers, particularly open-source or lower-cost solutions, further reducing market dominance.

- Perceived Favoritism: Prioritizing first-party applications could lead to accusations of unfair practices, such as preferential treatment for proprietary integrations over third-party developers.

Impact: To maintain trust and loyalty, foundation model pioneers need to strike a delicate balance between pursuing first-party applications and supporting third-party developers with robust tools, APIs, and partnerships.

3. Integration Complexities

Building successful applications often requires seamless integration with broader enterprise ecosystems, posing significant technical and strategic challenges:

- Enterprise System Integration: Applications must work effectively with existing enterprise software (e.g., CRMs, ERPs, and communication tools) to deliver value. Achieving this requires extensive customization and partnerships with enterprise solution providers.

- Cloud Ecosystem Dependencies: Many applications rely on cloud infrastructures like AWS, Azure, or Google Cloud. Ensuring compatibility and performance across these platforms adds a layer of operational complexity.

- Data and Privacy Concerns: Enterprise customers demand robust data handling, privacy, and compliance measures. Building applications that meet stringent requirements for data governance can slow development and increase costs.

- Scalability and Reliability: Applications must scale seamlessly to accommodate enterprise demand while maintaining performance and reliability. This requires significant investment in infrastructure and engineering.

Impact: The technical and operational complexity of integration raises costs and extends development timelines, potentially delaying time-to-market and reducing the competitiveness of new applications.

4. Brand and Focus Dilution

Expanding into applications could dilute the strategic focus of foundation model pioneers:

- Shift in Priorities: Balancing the development of foundational models with the demands of application development may overstretch resources and create internal conflicts over priorities.

- Reputation Risk: A misstep in the application space—such as a poorly received product—could harm the brand reputation of pioneers known for their technical excellence in foundational models.

Impact: Companies must clearly define their strategic objectives and ensure that their application efforts complement, rather than detract from, their core capabilities in foundational models.

Looking Ahead: Generative AI’s Application-Driven Future

The pivot toward the application layer reflects a broader evolution in the generative AI ecosystem. Just as software and applications became the dominant forces in the mobile and cloud industries, AI-driven applications are poised to become the primary growth engines for foundation model pioneers. The potential for innovation is vast, ranging from personal productivity tools to specialized enterprise solutions.

However, the transition will require strategic navigation. Foundation model pioneers must leverage their unique capabilities, maintain strong relationships with current partners, and deliver compelling use cases that justify their place in the application layer. Success will depend on their ability to balance innovation with collaboration while navigating the competitive pressures of an increasingly crowded market.

In this new era, the application layer is no longer just a complement to foundational models—it is the central frontier for generative AI growth, innovation, and value creation.

The Economics of Generative AI

A detailed analysis of the Gen AI ecosystem reveals a stark contrast with the traditional cloud market. Semiconductors currently dominate the value chain, capturing 83% of total revenues ($75 billion annually) and 88% of gross profits. In comparison, the application layer generates a modest $5 billion annually, with gross margins of 50-55%.

However, as the market matures, this dynamic is expected to shift. Applications are projected to capture a larger share of both revenue and profit over the next decade. Historical precedents, such as the evolution of the cloud ecosystem, suggest that applications will eventually become the largest driver of value in the AI stack.

Shifting Market Dynamics: Risks and Opportunities

The move toward applications is not without risks. Foundation model pioneers face the challenge of competing with their own customers, many of whom have built successful businesses around using AI models to power specialized applications. Additionally, as AI applications evolve, they will require deeper integration with cloud infrastructures, further blurring the lines between cloud and AI ecosystems.

Key Predictions for 2025 and Beyond

- Market Consolidation: As hardware costs stabilize and open models become more sophisticated, smaller players may be acquired or exit the market.

- Increased Collaboration: Foundation model pioneers may partner with hyperscalers like AWS and Google Cloud to integrate their applications into broader cloud ecosystems.

- Differentiated Offerings: Customization and vertical-specific solutions will become key to sustaining competitive advantage in the application layer.

The Bottom Line

The generative AI industry is undergoing a fundamental shift, moving from the development of foundational models to a focus on applications that deliver concrete value to businesses and consumers. This transition reflects the maturity of the ecosystem and the growing recognition that applications, with their potential for higher margins, differentiation, and direct customer engagement, will drive the next phase of growth.

For businesses, this shift presents both opportunities and challenges. Success will require decisive action: investing in AI applications that align with strategic goals, collaborating with partners to build complementary capabilities, and creating solutions that address real-world needs. These steps are critical to staying competitive in an increasingly application-centric market.

The application layer is set to become the dominant driver of growth and profitability within the generative AI ecosystem over the next decade. Companies that act now to develop innovative, user-focused AI solutions will not only capture emerging opportunities but also secure a leadership position in this evolving landscape. To thrive in this transformation, businesses must start building today—because the future of generative AI is here.

** Credit to Apoorv Agrawal who inspired some of the content in this prediction and from whom some of the infographics are derived.